Cash Secured (Covered) Puts (Put-Write) Strategies in DeFi — Measuring Performance Using Stablecoins and using Layer 1 Tokens

Wouldn’t it be nice to find a way to generate yield without that yield being paid in s**tcoins, or taking on the credit risk of lending our coins out to different protocols? That’s where option strategies, like the covered calls and put write strategies, comes in. (Check out my previous article on using options as sustainable yield in DeFi). Check out this article and this article on Covered Call strategies. And this article on yield farming if you are curious.

What is a Put Option

Cash Covered Put strategies involve writing (selling) put options. But what is a put option? A put option is an agreement between 2 parties. The buyer pays a premium in order to have the option to sell the underlying asset (ex. SOL) at a certain price (aka strike price) on (or by) a certain date (aka expiration date). The seller receives the premium and is on the hook to buy the underlying asset (SOL) at that strike price if the option buyer executes the option.

So for example, let’s say SOL is at $150, the strike is $100, the premium is $10 and the expiration is 1 week from now. The buyer would pay the seller $10 hoping that the price of SOL at the expiration is less than $100 1 week from now. The buyer starts to make a profit if the price of SOL is less than $90 ($100 strike minus the $10 premium they paid for the option). The seller keeps all $10 if the price of SOL stays above $100 1 week from now. The seller gets yield by giving the buyer this option. The option is more expensive the more volatile the underlying asset is. Therefore, the seller is ‘short’ vol (because the value of being long the option increases as implied volatility increases), and harvesting that volatility premium.

What is a Cash Covered Put

A Cash Covered Put strategy involves selling a put option and locking up all of the necessary ‘cash’ (or whatever tokens the protocol requires) needed to buy back the underlying if the put option is executed. So in the example above, we would need to lock up $100 USDC in the contract in order to write that put option. Understanding the performance of a cash covered put strategy really depends on what you define as your ‘numeraire’, or base currency/token. The performance of this strategy differs depending on what token you base your performance. Let’s go through a stylized example with 3 different scenarios, each looking at an investor with a USDC base, and a SOL base.

Stylized Example Setup

Let’s say you own 1 SOL right now at $150 (so the cost basis is $150), and you write the same put as above (strike is $100, premium is $10, expiration is 1 week from now). I am going to assume that you immediately swap your 2/3 of your SOL into USDC to cover the cash of writing the put (you need to sell 100 USDC worth of SOL currently priced at 150, so sell 2/3 of your SOL for USDC). So the assets you use for this trade (you basis for performance) are 100 USDC, or 0.667 SOL.

Just as a note, I personally believe that the correct way to look at this is through a USDC (stablecoin) lens. Swapping out of the underlying, to lock up the stablecoin in a cash secured put, then using the underlying as your numeraire, seems wrong to me. But I wanted to include both views in case someone does think of the world this way.

Scenario 1

SOL expires at 150 USDC, so the put expires worthless. SOL has move 0% versus USDC

USDC Base — You collect $10 USDC as the premium

- At expiration, the price of SOL doesn’t move. In this case, the written put expires worthless, so you keep the 100 USDC that was locked in the contract and the premium of 10 USDC. So the total P&L = 10 USDC.

- Total performance gross of fees = 10 / 100= 10% (10 USDC)

SOL Base — You collect 10/150 = 0.0667 SOL (6.67% yield) gross of fees

- At expiration, the price of SOL doesn’t move. In this case, the written put expires worthless, so you keep the 100 USDC and the premium of 10 USDC. You then flip that 110 USDC back into SOL at a price of 150, which gives you 0.733 SOL. Your P&L in SOL = 0.733–0.667 = 0.0667 SOL.

- Total performance gross of fees = 0.733 / 0.667 –1 = 10% (0.0667 SOL)

Scenario 2

SOL expires at 75, so the put option expires in the money, and the put is exercised. SOL has moved -50% vs USDC

USDC Base — You collect 10 USDC as the premium, but have to buy the SOL at the strike price of 100. You then sell the SOL on the market at the price of 75 to get back to all USDC.

- At expiration, the written put is executed. You keep the premium of 10 USDC. You use the cash secured in the contract to buy the SOL at the 100 strike price, then sell that 1 SOL on the market at the market price of 75. So your P&L = 10 + 75–100 = -15 USDC.

- Total performance gross of fees = -15 / 100 = -15% (-15 USDC)

SOL Base — You collect 10 USDC as the premium and convert that to 0.133 SOL (10/75), you receive 1 SOL because the put option is executed

- At expiration, the written put is executed. You receive 1 SOL (you purchase at the 100 USDC strike price using the 100 USDC locked in the contract). You convert the 10 USDC premium into SOL at the market price of 75, to get 0.133 SOL. Your total SOL is 1.133. Your P&L in SOL = 1.133–0.667 = 0.467 SOL

- Total performance gross of fees = 0.467 / 0.667= 70% (0.467 SOL)

Scenario 3

SOL expires at 225 USDC, so the put expires worthless. SOL has move 50% versus USDC

USDC Base — You collect 10 USDC as the premium

- At expiration, the price of SOL has increased by 50%. In this case, the written put expires worthless, so you keep the 100 USDC that was locked in the contract and the premium of 10 USDC. So the total P&L = 10 USDC.

- Total performance gross of fees = 10 / 100= 10% (10 USDC)

SOL Base — You collect 10 USDC as the premium and convert that to 0.044 SOL (10/225), you convert the 100 USDC that was locked into the contract into SOL when the put expires worthless and your locked USDC is released, which equals 0.44 SOL (100/225).

- At expiration, the written put expires worthless. You convert the 10 USDC you receive as premium and the 100 USDC that is now unlocked (because the put expired worthless) into 0.489 SOL (110/225). You P&L = 0.489–0.667 = -0.1778 SOL

- Total performance gross of fees = -0.1778/ 0.667= -26.67% (-0.1778 SOL)

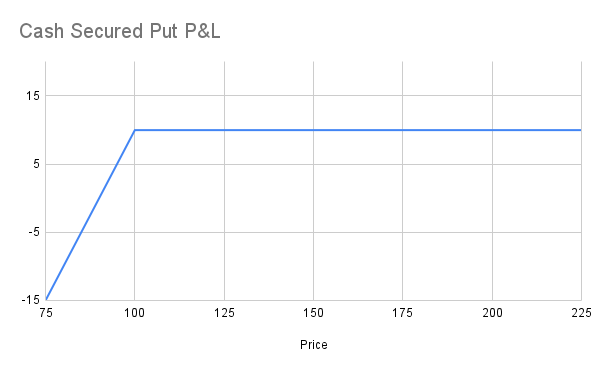

Graphs of P&L in USDC Base

You can see the P&L of just locking up 100 USDC into a cash secured put. As long as the price of SOL is greater than the strike price of the put, you get to keep your premium. You start to have negative P&L when the price of SOL is less than the strike minus premium (90 = 100–10).

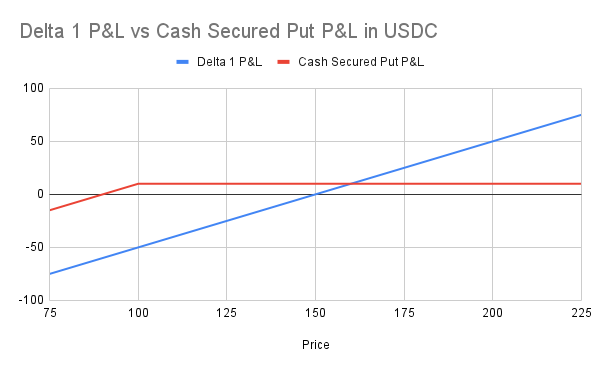

You can see how the P&L of the Cash Secured Put strategy performs relative to just buying and hodling the 1 SOL at $150 below. The Cash Secured Put strategy outperforms as long as the price at expiration is less than you SOL basis plus Premium ($150 + $10 = $160). If the price of SOL at expiration 1 week from now is higher than $160, you would have been better off just hodling the SOL and not converting part of the SOL into USDC to lock into the contract and writing the put option. But as long as the price of SOL is below that $160 mark 1 week from now, you are better off swapping some of the SOL into USDC and writing a cash secured put.

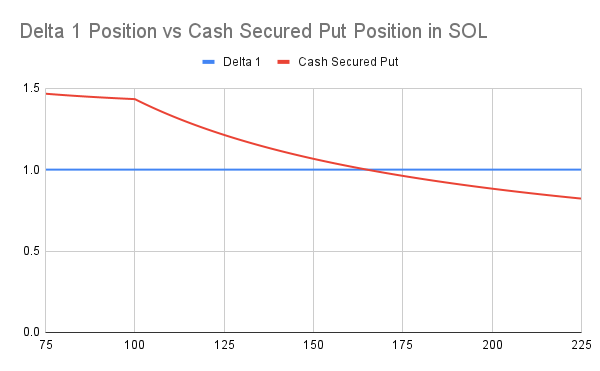

Graph of P&L in SOL Base

Here is the same view of a cash secured put, but instead of basing it in USDC, this is based in SOL. This is slightly confusing because the assumption here is that you start with 1 SOL priced at 150 USDC, then you sell 2/3 of that SOL at 150 USDC (for 100 USDC), then you will buy back SOL. So you end with more SOL as the price of SOL decreases. You can see a strong kink in the cash secured put (red line) at the strike price. This is because any price below 100 you receive 1 SOL at 100 USDC. Only the 10 USDC premium is converted back into SOL at a lower and lower price (as the price of SOL goes below the strike price of 100)

This can be a complicated strategy to run on your own

To be successful in implementing a cash secured put strategy, you need to make a lot of decisions. What strikes of puts should I sell? How many puts should I sell? What expiration of puts should I sell? What protocol should I use for put writing? Do I need to be fully collateralized (yes in the case of a cash secured put, but not necessarily for all put writing strategies)? Am I getting good quotes for selling these puts? What happens if the put option actually gets exercised, do I need to actually deliver the underlying, or settle the position in a different token?

All of these are important points to consider when implementing any option strategy. This is why many people don’t even think about these types of things. BUT, there are some new protocols out there that are bringing these types of strategies to the masses! My personal favorite is Friktion. The team has a strong background, they recently launched mainnet, and they already crossed the $100M TVL mark.

If you are interested in these types of strategies, want yield but don’t want to have to make all of the decisions around trading options, and the constant monitoring, you can just deposit into Friktion Volts #2 and let them do the rest!

Conclusion

I hope this helps explain what a cash secured put is, and why teams like Friktion are bringing these strategies to the masses. It’s important to know the risks you are taking when participating in different DeFi strategies. Many times it’s not obvious and you really do have to DYOR. But it definitely is possible to make some money out there, and in this constant search for yield, new asset management protocols like Friktion will continue to bring you new strategies to use.

Good luck and happy degening!

About the Author

For full disclosure I mostly use Solana for DeFi, because I don’t have enough assets to justify Ethereum gas fees. I have a little bit in Algorand, Cardano and Polkadot DeFi. I am actively involved in multiple Friktion volts and a contributor in their Discord, and am beta testing Dappio Wonderland 🐰.

I am invested in SOL, ADA, ETH, DOT, ALGO, MIOTA along with plenty of other tokens.

This is not Financial Advice!